Key takeaways

Rho is the strongest Mercury alternative: one platform for banking, cards, bill pay, expenses, and treasury at $0 - no minimums, no per-user fees.

Mercury works early, but the constraints add up: $250K for treasury, $15K for monthly card repayment, no AP automation at any tier.

Match the platform to your model: integrated stack - Rho. Global multi-entity - Brex. Spend on top of existing bank - Ramp. Cash bucketing - Relay. Startup-native chartered bank - Grasshopper or SVB.

For most venture-backed startups, Rho is the strongest Mercury alternative - combining everything Mercury does plus corporate cards with no minimum balance, bill pay, expense management, and treasury in one integrated platform at $0 per user.

If you're searching for a Mercury alternative, you're asking one of two questions.

Either you're evaluating Mercury against other options and trying not to land somewhere you'll have to rebuild from in eighteen months. Or you're already on Mercury, the company has grown, and a finance hire just asked why banking, cards, expense management, and bill pay are all in different places.

Both questions have the same underlying answer: Mercury is a genuinely strong financial product. It's not a complete financial stack.

Mercury is where founders go for the fastest possible start - and there's real value in that. The onboarding is clean, the interface is honest, and for a pre-product company with $500K in the bank and no finance team, it does the job.

The question isn't whether Mercury works at inception.

The question is what happens at month six, when you're managing payroll, vendor invoices, team cards with spend limits, and a treasury allocation - and each of those things lives somewhere different.

Here are the 13 strongest Mercury alternatives in 2026, what each is actually built for, and how to choose based on where you are.

Why founders look past Mercury in 2026

Mercury is a dependable banking platform for startups, but there are a few reasons why companies opt for alternatives.

1. No dedicated support - unless you pay $299/month

Mercury has no phone support on any tier. At Rho, you can always reach a real person - because Rho is built as a relationship bank, not a ticket system.

This is the biggest difference between the two platforms - and the one that matters most when something actually goes wrong.

Mercury's support model is chat only - no phone support exists on any Mercury plan. Mercury does not publish response time commitments on any tier.

A dedicated relationship manager - someone who knows your account, understands your business, and can act on your behalf - costs $299/month on Mercury Pro (billed annually; per Mercury’s pricing page, May 2026; subject to change). Below that, you're on shared chat support with no dedicated contact.

Rho is built differently. The model isn't "submit a ticket and wait" - it's "there's a real person available to you, always."

Early-stage accounts get live human support via in-app chat with under-a-minute average response times, 24/7, at no cost. Growth-stage and larger accounts get dedicated coverage - a named team including a Customer Experience Manager, Account Manager, and Account Executive who know your company, your cash flow, and your financial operations.

The philosophy behind this is intentional. Rho's premise is that banking shouldn't feel like enterprise software support.

When a founder discovers a failed wire at 11pm before Monday payroll, the answer isn't a ticket number. It's a person.

For a first-time founder managing real capital for the first time, this is often the thing they don't think about until they need it. And when they need it, it's the only thing that matters.

2. Advanced features require a paid plan

Enriched NetSuite automations, reimbursements for more than 5 users, and a relationship manager are paywalled behind Mercury Plus ($29.90/month, billed annually) or Pro ($299/month, billed annually). Rho includes all of this at $0.

The free Mercury account covers checking, savings, basic bill pay, IO card access, and basic expense management including reimbursements for up to 5 users/month. Growing companies quickly hit the paywall:

Enriched NetSuite automations → Mercury Pro required (per Mercury’s pricing page, May 2026)

Multiple GL codes for bill payments → Mercury Plus ($29.90/month, billed annually)

Reimbursements for more than 5 users/month → Mercury Plus; $5/additional active user above 20 on Plus

Dedicated relationship manager → Mercury Pro only ($299/month, billed annually)

For a 20-person company, Mercury Pro alone costs $299/month before any additional tools.

Total cost to match what Rho provides at $0 - including AP automation depth and treasury access - can reach $400-$600/month depending on the plan and tools added.

3. Significant balance requirements unlock the full product

Monthly card repayment terms require $15K in Mercury. Treasury requires $250K. Rho has no balance requirements for any feature.

Mercury's product tiers based on account balance:

$15,000 → unlocks IO Mastercard monthly repayment terms (daily repayment applies below this threshold)

$50,000 → qualifies for the premium metal IO card

$250,000 → required to access Mercury Treasury

A founder who raised a $500K seed and wants to earn yield on idle cash must hold half their capital in Mercury just to qualify.

Rho Treasury has no minimum balance and is available from day one.

4. Mercury is still becoming a bank - and that's worth understanding

Mercury is a fintech company, not a bank. It operates through partner banks - Choice Financial Group and Column N.A. - that hold your deposits. Mercury received conditional OCC approval to establish Mercury Bank, N.A. in April 2026, but that charter is not yet active and has no confirmed activation timeline.

Most founders don't realize this when they open a Mercury account. Mercury is the interface - the dashboard, the card, the brand.

The actual money lives at partner banks, not Mercury itself.

Conditional OCC approval is a meaningful step forward, but it isn't a charter. The FDIC and Federal Reserve still need to sign off before Mercury Bank can legally open. It could happen in late 2026. It could be later. There's no public timeline.

For most early-stage founders, this doesn't change day-to-day operations. Where it starts to matter: when you're holding $1M+ post-raise, when a board member or investor asks where the cash sits, or when you're choosing a financial foundation you expect to still be on at Series B.

Rho's banking partner - Webster Bank, N.A., founded in 1935 with $85.6B in assets - is a settled institutional answer to that question. Mercury's is still in progress.

5. Expense management is basic and caps quickly

Mercury has card controls, receipt matching, and reimbursements - but no AP automation, no multi-step approval workflows, and no procurement routing. Free reimbursements cap at 5 active users/month, above which a paid plan is required. Founders who need the full spend management stack still add separate tools.

Mercury's expense management covers: reimbursements (free for up to 5 active users/month), receipt policies and matching, IO card spend controls, category restrictions, and GL code categorization. QuickBooks and Xero enriched automations are free; NetSuite categorizations require Pro.

What it doesn't include: AP automation with vendor invoice processing, multi-step approval workflows for procurement, or the integrated bill pay + expense + treasury stack that Rho provides natively.

For a team beyond five employees submitting expenses, you're on a paid plan. For a team that needs procurement governance or complex approval routing, you're adding separate tools.

That's the patchwork Rho was built to replace.

6. The IO Card has a $15,000 threshold for full benefits

Mercury's IO card is available from day one with no minimum balance. To unlock monthly repayment terms and higher limits, you need $15K in Mercury. The $50K figure only applies to the premium metal physical card.

Mercury's IO Mastercard is a charge card with unlimited 1.5% cashback and no personal guarantee. It's available to eligible customers from the moment they open an account - but the 1.5% cashback and monthly repayment terms both require a $15,000 Mercury balance. Below that threshold, the card uses daily repayment and cashback does not apply.

The structure works like this: the IO card is accessible from day one, but daily repayment applies and cashback is not available until your Mercury balance reaches $15,000. Once you hit that threshold, monthly repayment terms unlock and 1.5% cashback activates.

The $50,000 figure applies only to qualifying for the premium metal physical IO card - not to accessing IO itself.

For a pre-seed founder who just raised a $500K SAFE, Mercury's IO card is accessible. The practical limitation for early-stage founders isn't the card threshold - it's the treasury minimum.

Mercury Treasury is only available to accounts with $250,000 or more across all Mercury accounts - meaning a founder who just raised $500K needs to park half their capital in Mercury just to earn yield on the rest.

Rho Treasury is available with no minimum balance requirement from the day you open your account, with multi-asset portfolios across T-Bills, Morgan Stanley (MULSX), and Vanguard (VFSTX) funds.

Mercury alternatives compared

Platform | Best for | Key features | FDIC coverage |

|---|---|---|---|

Rho | The default financial platform for venture-backed startups - banking, cards, bill pay, expenses, and treasury in one place at $0 | Checking, cards, vendor cards, treasury, bill pay, invoicing, expenses, accounting | Up to $75M (ADM network) |

Brex | Global, multi-entity scale | Cards, travel, multi-entity, AI automation | Up to $6M (24 partner banks) |

SVB | Startup relationship banking with VC network access and venture debt | Checking, savings, SVB Innovator Card, venture debt, cash management, global payments | $250K standard (First Citizens Bank, Member FDIC) |

Grasshopper | Digital bank with extended FDIC coverage and high-yield savings for startups | Checking, savings, debit card, bill pay, investor network access, venture lending | Up to $125M (ICS sweep network) |

Relay | Multi-account cash management and team budgeting | Up to 20 checking accounts, team permissions, automated transfers | Up to $3M (Thread Bank sweep program) |

Ramp | Spend management on top of an existing bank | Cards, expense management, bill pay, procurement, business account | Standard $250K (First Internet Bank) |

Bluevine | High-yield checking and credit access | High-yield checking, bill pay, line of credit up to $250K | Up to $3M (sweep network) |

Slash | Digital-first businesses (e-commerce, affiliate, crypto) wanting uncapped cashback and AI banking | Checking, uncapped cashback cards, expense management, treasury, global payments, stablecoin, AI agent | Hundreds of millions (Column N.A. + IntraFi 800+ bank sweep) |

Novo | Freelancers and very small teams | No-fee checking, unlimited transactions, ATM refunds | $250K (Middlesex Federal Savings) |

Chase | Traditional banking relationship and physical branches | Branch network, lending, credit cards, merchant services | $250K standard |

Found | Solo founders needing banking + bookkeeping + taxes | Built-in bookkeeping, tax estimates, banking | $250K (Piermont Bank) |

1) Rho - Best Overall

![]()

The institutional foundation is Webster Bank, N.A., an $85.6 billion commercial bank founded in 1935 and joining Banco Santander to form a top-10 US bank by combined assets.

That's a different category of institution than the partner banks behind most fintech-led banking products, and it matters when an investor, board member, or finance hire eventually asks where the company's cash sits.

Rho is now available at incorporation through both Stripe Atlas and Clerky. Founders incorporating with Stripe Atlas can open a Rho account before their EIN arrives, issue cards, and configure their finance stack while company formation is still in progress. Clerky users can pre-fill a Rho application with one click from their incorporation paperwork.

The customer roster is the proof. Perplexity runs treasury on Rho. Dr. Squatch and Rhode Skin both scaled successfully on the platform.

Rho serves over 5,000 customers managing more than $2 billion in AUM, with over a dozen publicly traded companies running their finances on it.

How Rho compares to Mercury

1. Banking plus the complete financial stack. Mercury is a banking product with cards, basic expense management, and bill pay. Rho is a banking product with corporate cards (available from day one, no minimum balance), bill pay, full expense management with AP automation, invoicing, and treasury - all connected, all at $0. The workflow that takes a Mercury founder multiple tools to complete takes a Rho founder one.

2. Cards accessible from day one with no minimum balance. Rho's corporate cards are available from day one with no minimum balance required, no personal guarantee, and up to 1.5% cashback from day one. Mercury's IO Mastercard is also available from day one - but the 1.5% cashback and monthly repayment terms both require a $15,000 balance. $250,000 is required to access Mercury Treasury.

3. The institution holding your money. Webster Bank, N.A. - $85.6 billion, founded 1935, joining Banco Santander. Mercury operates through partner banks (Choice Financial Group and Column N.A.) that hold deposits today. Mercury Bank, N.A. received conditional OCC approval in April 2026 but is not yet an active chartered bank.

4. Support that's actually available. Rho's average customer support response time is under a minute, 24/7, with a real person, included from day one. Mercury has no phone support on any tier.

5. Full platform at $0. Everything - multi-entity, ERP integrations, AP automation, expense management, treasury - at no per-user cost. Mercury gates enriched NetSuite automations and advanced features behind Plus ($29.90/month, billed annually) and Pro ($299/month, billed annually).

Rho at the pre-seed stage

Most of the platforms in this comparison are evaluated by finance hires. Rho is often evaluated by the founder alone, in the first week of operations - before there's a CFO, a controller, or even a full-time employee. That's not an edge case. That's the customer Rho was built for.

Opening the account. Rho supports pre-EIN onboarding - the account can be open before your EIN arrives. A founder who just incorporated through Stripe Atlas and signed a $500K SAFE can have a Rho account live, a card issued and earning up to 1.5% cashback, and treasury ready for when the funding lands. No minimum balance. No waiting period. Founders who've gone through it describe expecting an hour and finishing in 20 minutes.

Getting a card. Cards are issued immediately with no minimum balance and no personal guarantee. Mercury's IO Mastercard is also available from day one on an introductory basis - though you need $15,000 in Mercury to unlock monthly repayment terms and higher limits.

Putting idle cash to work. The moment your funding lands, Rho lets you move idle cash into treasury from the same dashboard where you bank - with no minimum balance required. Mercury Treasury requires a $250,000 minimum balance across all Mercury accounts, meaning a founder who just raised a $500K seed round needs to hold half of their capital in Mercury just to access yield. Rho Treasury has no such threshold.

Support that responds like a partner. 32-second average response time via in-app messaging, from day one, at no cost. For a first-time founder managing their first real capital, that's not a feature - it's the whole point.

What Rho looks like as you scale. The same account that holds your first $500K SAFE handles your first payroll run, your first batch of vendor payments, your first treasury allocation, and your first month-end close with a finance hire. You don't migrate at Series A. The foundation scales with the company.

Rho key features

Business Checking - Provided by Webster Bank, N.A. with no monthly fees, no minimums, $0 same-day ACH, $0 domestic wires

Up to $75M FDIC insurance - Through partner banks via the ADM network

Corporate Cards - Up to 1.5% cashback on all purchases with Rho Platinum; available from day one with no minimum balance; plus dedicated Vendor Cards for every subscription

Bill Pay - Pay hundreds of vendors in minutes with zero platform fees

Invoicing - Send invoices and get paid from where you bank

Expense Management - Connect Gmail once and Rho captures every receipt automatically, matched to the right transaction

Rho Treasury - Multi-asset portfolios with selectable allocation modes and automatic reinvestment

Accounting Integrations - Direct sync with QuickBooks Online, NetSuite, Sage Intacct, and more

Available at incorporation - One-click setup through Stripe Atlas and Clerky

Rho Partner Portal - Built specifically for fractional CFOs and accounting partners

24/7 support - Live human support from day one with average response times under a minute via in-app chat

Rho pricing

$0 monthly plans

$0 per-user fees

$0 same-day ACH

$0 domestic wires

$0 support

$0 platform fees on bill pay

$0 access to AP, Expense, and Accounting Automation

The only fee: 1% on foreign currency transfers.

What customers say

"Better spend management, better customer service, easy migration, higher treasury, better incentives. Much less admin time spent on spend tracking, easier card management than we had with the other guys."

— Skyler Ji, Co-founder, Spark (YC-backed startup, migrated from Mercury)

"The company implementation of Rho was easy and took less than 2 hours. We sync with QuickBooks Online seamlessly, which has saved the finance department 60 hours per month."

— Verified Rho customer, G2

For more detail, see Rho vs. Mercury.

Where Rho isn't the right fit

If your primary need is global card issuance in 20+ currencies for a multi-entity team, Brex is purpose-built for that.

If your finance team's biggest pain is procurement governance with PO matching across hundreds of vendors, Airbase is the specialized tool.

If you're a solo founder or freelancer with no team and minimal vendor activity, Mercury or Found may be simpler starting points. Rho is built for the founder picking their financial foundation and the company growing into a serious operation.

See it for yourself — get a demo in 20 minutes →

2) Brex

Brex is a strong Mercury alternative if your needs are global. Multi-entity card issuance, integrated travel booking, AI-driven expense automation, and operations in 50+ countries make it the right tool for companies operating across borders at scale. Brex serves over 25,000 companies as of 2026.Brex key features

Brex is a strong Mercury alternative if your needs are global. Multi-entity card issuance, integrated travel booking, AI-driven expense automation, and operations in 50+ countries make it the right tool for companies operating across borders at scale. Brex serves over 25,000 companies as of 2026.Brex key features

Corporate Cards - Global acceptance with AI-powered policy controls across 210+ countries and territories

Expense Management - Auto-generated receipts, pre-populated memos, AI categorization

Travel Management - In-app booking with policy enforcement and 24/7 travel support

Bill Pay - AI-driven invoice capture, coding, and approval workflows

Banking and Treasury - Up to $6M FDIC insurance, competitive yield on operating cash

AI assistant integrations - Brex in ChatGPT and Brex in Claude for natural-language queries

Brex pricing

Essentials: $0/user/month — global cards, AI-powered rules, accounting integrations

Premium: $12/user/month — customizable expense policies, advanced approvals, multi-entity

Enterprise: Custom pricing

Honest assessment

Capital One completed its $5.15 billion acquisition of Brex on April 7, 2026. For founders who originally chose Brex as the modern alternative to big-bank infrastructure — Brex is now part of the largest US card issuer. That's a relevant institutional fact worth considering.

For global multi-entity companies, the platform itself remains the strongest in this list. For early-stage US-based startups comparing Mercury to Brex, the feature surface is broader than most early-stage moments require, and per-user pricing at $12/month adds up quickly as the team grows.

Not ideal for: Early-stage US-based founders who don’t need cross-border card issuance, are sensitive to per-user pricing, or originally chose fintech-native banking specifically to stay outside big-bank infrastructure. (Note: Brex is now a Capital One subsidiary.)

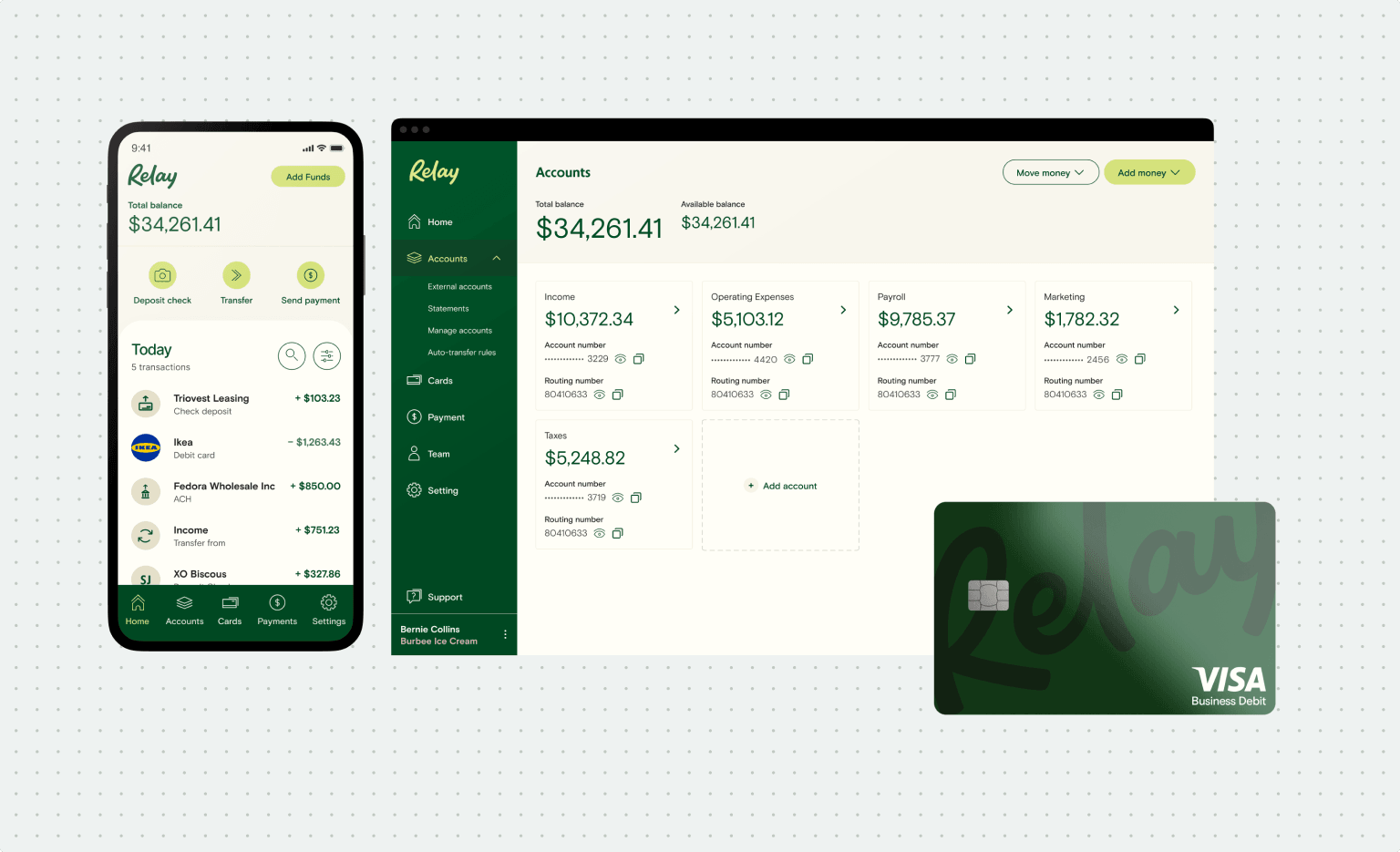

3) Relay

Relay is a business banking platform built around multi-account cash management. Its core proposition: organize your cash into up to 20 checking accounts by purpose — payroll, operating expenses, reserves, taxes — and manage team spending permissions from one dashboard. It's the most structured cash management tool in the startup banking category and genuinely useful for founders who think in buckets.

Relay key features

Up to 20 checking accounts — Separate operating cash by purpose without juggling multiple banks

Team permissions — Role-based access, individual spending limits, and approval workflows

Automated transfers — Rules-based sweeps between accounts

Debit and physical cards — One card per team member with individual limits

Accounting integrations — QuickBooks Online and Xero

Relay pricing

Relay: $0/month — up to 20 checking accounts, team permissions, 2 debit cards

Relay Pro: $30/month — additional cards, accelerated ACH, auto-import of bills, dedicated support

Honest assessment

Relay is FDIC-insured through Thread Bank, Member FDIC, for up to $250K per depositor. Relay is the right tool for a bootstrapped or early-stage team whose primary pain is cash flow visibility and budget discipline — and whose needs stop at the bank account. It does not offer corporate charge or credit cards, AP automation, expense management, or treasury yield in any meaningful form. For a venture-backed company that needs cards, bill pay, and expense management alongside banking, Relay is a partial answer. For a small team that wants to run a tight cash envelope system without a finance hire, it's genuinely good.

4) Ramp

Ramp is a spend management platform that extended into banking through a Business Account powered by First Internet Bank of Indiana (Member FDIC) via Increase's API infrastructure. It's the right Mercury alternative if your primary pain is spend management automation — corporate cards, expense management, procurement, and AP — and you're willing to manage your banking relationship alongside it.

Ramp key features

Corporate Cards — Up to 1.5% cashback, AI-powered spend controls and policy enforcement

Expense Management — Automated receipt capture, categorization, and approval routing

Bill Pay — Vendor payments via ACH and check (Standard ACH $0.59/transaction, Check $1.99/transaction, effective June 1, 2026; waived with Ramp Business Account)

Procurement — Purchase request routing, vendor onboarding, PO matching (Ramp Plus)

Ramp Business Account — FDIC-insured checking via First Internet Bank of Indiana, accessed through Increase

Treasury — Investment Account and Managed Investment Account (not FDIC-insured)

Accounting integrations — QuickBooks, NetSuite, Xero, Sage Intacct

Ramp pricing

Starter: $0/month — cards, expense management, basic AP

Core: $0/month — full expense automation, basic accounting sync

Plus: $15/user/month — multi-entity, advanced procurement, deeper ERP integrations

Enterprise: Custom

Honest assessment

Ramp is the right answer for a company that already has a banking relationship it trusts and wants to add a best-in-class spend management layer on top. The product surface area has expanded significantly — cards, expense management, bill pay, procurement, travel, a business account, investment accounts, several AI agents — which makes it more powerful and more complex simultaneously. For a CFO at a 200-person company, that breadth is a feature. For a founder without a finance team evaluating this against Mercury, it can be more than the moment requires.

The institutional question: Ramp's Business Account uses First Internet Bank of Indiana, a ~$5.6 billion internet-only bank. For founders who care about the institution holding their cash, that's worth understanding relative to Webster Bank's foundation under Rho.

5) Bluevine

Bluevine is a business banking platform built primarily for small and medium-sized businesses that want meaningful yield on operating cash and access to a revolving credit line. It's the strongest Mercury alternative if your primary need is earning interest on your checking balance and having a credit option available.

Bluevine key features

High-yield checking — Up to 3.0% APY on Premier plan (variable; subject to change); Standard plan earns 1.3% APY only if monthly activity goals are met, otherwise 0.00%

Bill Pay — Up to 5 paid bills/month on Standard; unlimited on higher plans

Sub-accounts — Organize cash by purpose within one account

Line of credit — Revolving credit up to $250K

Debit Mastercard — Standard debit card, no cashback credit card option

Bluevine pricing

Standard: $0/month

Plus: $30/month

Premier: $95/month

Honest assessment

Bluevine is built for small business owners, not venture-backed startups. It doesn’t offer corporate cards, AP automation, or expense management. For a funded startup evaluating Mercury, Bluevine’s feature set stops short of what a company with real financial operations typically needs within the first year.

Bluevine is optimized for a specific founder profile: one who prioritizes yield on operating cash and may need credit access, and whose primary need is checking rather than cards or spend management. It doesn't offer corporate cards, AP automation, expense management, or treasury in any form that competes with Rho or Mercury. For a venture-backed startup with a real financial operations need, Bluevine is a partial answer. For a small business owner whose primary pain is earning something on idle cash without moving it — and who needs a credit line available — it's purpose-built.7) Novo

Novo is a business banking platform built for freelancers, solopreneurs, and very small businesses. Its core value proposition is simplicity: free checking, unlimited transactions, ATM fee refunds, and a clean mobile interface.

Novo is a business banking platform built for freelancers, solopreneurs, and very small businesses. Its core value proposition is simplicity: free checking, unlimited transactions, ATM fee refunds, and a clean mobile interface.

Novo key features

Free business checking — No monthly fees, no minimum balance, unlimited transactions

ATM fee refunds — Refunded on any ATM worldwide

Novo Boost — Early access to funds from Stripe and Square deposits

Reserves — Envelope-style savings buckets within one account

Accounting integrations — QuickBooks, Xero, Stripe, Square

Novo pricing

$0/month

Honest assessment

Novo is FDIC-insured through Middlesex Federal Savings, F.A., Member FDIC, for up to $250K. Novo is the right answer for a one-person operation that needs a clean, free checking account and nothing more. It does not offer corporate cards, treasury, bill pay automation, or expense management. For a venture-backed startup with a real team and real vendors, Novo hits a ceiling immediately. It earns a place on this list because many early-stage founders look at it alongside Mercury — the honest comparison is that Mercury is more feature-rich than Novo, and Rho is more feature-rich than Mercury.

8) Chase

Chase for Business is the default recommendation for founders who need physical branches, handle cash deposits, or want a traditional lending relationship alongside their banking. It has nationwide branch coverage, business credit cards, and access to SBA loans — at the cost of slower onboarding, monthly fees, and no spend management integration.

Chase for Business is the default recommendation for founders who need physical branches, handle cash deposits, or want a traditional lending relationship alongside their banking. It has nationwide branch coverage, business credit cards, and access to SBA loans — at the cost of slower onboarding, monthly fees, and no spend management integration.

Chase key features

Business checking — Multiple account tiers with waivable monthly fees based on balance requirements

Physical branch network — Thousands of locations nationwide with ATM access

Business credit cards — Chase Ink line with rewards and travel benefits

Lending — Lines of credit, term loans, SBA loan programs

Merchant services — Payment processing for businesses accepting in-person payments

Chase pricing

$15–$95/month (waivable with balance or deposit requirements)

Honest assessment

Chase is FDIC-insured through JPMorgan Chase Bank, N.A., Member FDIC, for up to $250K per depositor per ownership category. Chase is the right answer for a company with physical cash handling needs, an existing Chase lending relationship, or investors who expect a big-bank name on the bank account. The onboarding takes days not minutes, the fees accumulate without meeting balance thresholds, and there is no integration with spend management or expense workflows. For a founder who just got funded and wants to move fast, Chase is not the starting point. For a company that has scaled, has complex cash deposit needs, and wants a full relationship bank — Chase makes sense as a complement, not a primary tool.

6) Found

Found is an all-in-one banking, bookkeeping, and tax platform built specifically for self-employed founders, freelancers, and one-person businesses. It automatically categorizes expenses, estimates quarterly taxes, and provides a simple interface that collapses banking and basic accounting into one product.

Found is an all-in-one banking, bookkeeping, and tax platform built specifically for self-employed founders, freelancers, and one-person businesses. It automatically categorizes expenses, estimates quarterly taxes, and provides a simple interface that collapses banking and basic accounting into one product.

Found key features

Free business checking — No monthly fee, no minimum balance

Built-in bookkeeping — Automatic expense categorization and profit/loss visibility

Tax estimates — Automatic quarterly tax calculations and payment reminders

Found card — Debit card with cashback on select categories

Basic invoicing — Send and track invoices from the Found dashboard

Found pricing

Found: $0/month

Found Plus: $19.99/month — advanced tax tools, priority support, bookkeeping reports

Honest assessment

Found offers FDIC insurance through Piermont Bank, Member FDIC, for up to $250K. Found is the right tool for a solo founder or freelancer whose biggest financial challenge is staying organized on taxes and understanding their cash position. It's not built for companies with teams, vendors, payroll, or real financial operations. The moment you hire your first employee or start paying multiple vendors, Found hits a hard ceiling. It earns a place on this list because founders evaluating Mercury as a solo operator sometimes land here — it's a legitimate choice for that specific context and a tool they'll graduate from quickly.

7) Airbase (now part of Paylocity)

Airbase is a procure-to-pay platform built for mid-market finance teams (100–5,000 employees) with sophisticated AP and procurement workflows. Now branded as "Airbase by Paylocity" and integrated with Paylocity's HCM platform under the "Paylocity for Finance" umbrella, Airbase pairs spend management with payroll and HR data on one system.

Airbase is a procure-to-pay platform built for mid-market finance teams (100–5,000 employees) with sophisticated AP and procurement workflows. Now branded as "Airbase by Paylocity" and integrated with Paylocity's HCM platform under the "Paylocity for Finance" umbrella, Airbase pairs spend management with payroll and HR data on one system.

Airbase key features

AI-Powered AP Automation — Touchless invoice processing with OCR

Guided Procurement — No-code approval routing for purchase requests

Corporate Cards — Virtual and physical with pre-approvals and ERP integration

ERP Integrations — NetSuite, Sage Intacct, QuickBooks, Microsoft Dynamics, Oracle

Unified HR + Finance data — Payroll and non-payroll spend through one Paylocity-backed view

Audit Trail — Compliance-ready documentation for every transaction

Airbase pricing

Custom pricing across Standard, Premium, and Enterprise tiers, with the Paylocity bundle increasingly the path to purchase.

Honest assessment

Airbase wins on procurement governance. It's not the system you'd open before you have a procurement problem to govern. For a 100+ person company with a finance team that needs PO matching, multi-step approval routing, and audit-grade procurement workflows — especially one already on Paylocity for HR — Airbase is purpose-built for that constraint. For a company comparing it to Mercury as a first banking platform, the complexity and pricing overhead aren't matched by the use case. File it for Series B and beyond.

8) SVB (Silicon Valley Bank)

Silicon Valley Bank is the most established name in startup relationship banking. Now a division of First Citizens Bank since its acquisition in March 2023, SVB banks more than 60% of the Forbes 2026 Fintech 50 and 40% of the Forbes 2025 AI 50. It's purpose-built for the innovation economy — with dedicated relationship managers, venture debt, and a network connecting founders to investors, accelerators, and VCs.

Important timing note: SVB is being rebranded as First Citizens Innovation Banking in Q4 2026 — as reported by Bloomberg. The banking products, relationship managers, and platform are unchanged — only the name is evolving.

SVB key features

Startup Banking (SVB Edge) — Free checking for the first 3 years, no monthly fees, no transaction fees, unlimited wires including FX, unlimited bill pay and mobile deposits

SVB Go — Digital banking platform custom-built for startups, available online and mobile

Startup Money Market — Up to 3.30% APY on qualifying balances (variable; as of svb.com/business-banking; subject to change)

SVB Innovator Card — Business credit card with 1.5x unlimited reward points on all purchases, no annual fee, no foreign transaction fees

Venture Debt — Debt solutions for Series A+ companies to extend runway and minimize equity dilution

Global Payments and FX — International payments in 90+ currencies with FX risk management tools

Accounting integrations — QuickBooks, Xero, Expensify

Ecosystem access — Connections to VCs, accelerators, and investor events; perks including AWS, MongoDB, Carta, and Slack credits

SVB pricing

SVB Edge (startup package): $0 for the first 3 years — no monthly fees, no transaction fees, unlimited wires and bill pay

Post-3-year pricing: contact SVB for account structure and fees

Venture debt: custom terms based on stage and use case

Honest assessment

SVB is the relationship banking option on this list. No other platform offers the same depth of VC network access, investor connections, or startup ecosystem infrastructure. For a founder raising a Series A or navigating a growth round who wants their bank to open doors — not just hold cash — SVB has a genuinely differentiated value proposition that Mercury, Rho, and most fintechs don't replicate.

The tradeoffs: FDIC coverage is standard $250K (First Citizens Bank, Member FDIC) — significantly lower than Rho's $75M or Grasshopper's $125M. SVB is not a spend management platform; there's no integrated expense management, AP automation, or bill pay controls at the depth of Rho or Ramp. The free banking period is limited to 3 years, after which pricing requires a conversation with a relationship manager. And for a pre-seed founder who just incorporated and needs to move fast, the relationship banking model is heavier than the moment requires.

Best used as the primary banking relationship for Series A+ companies that actively use SVB's VC network, venture debt products, or global payments infrastructure — often in combination with a spend management tool.

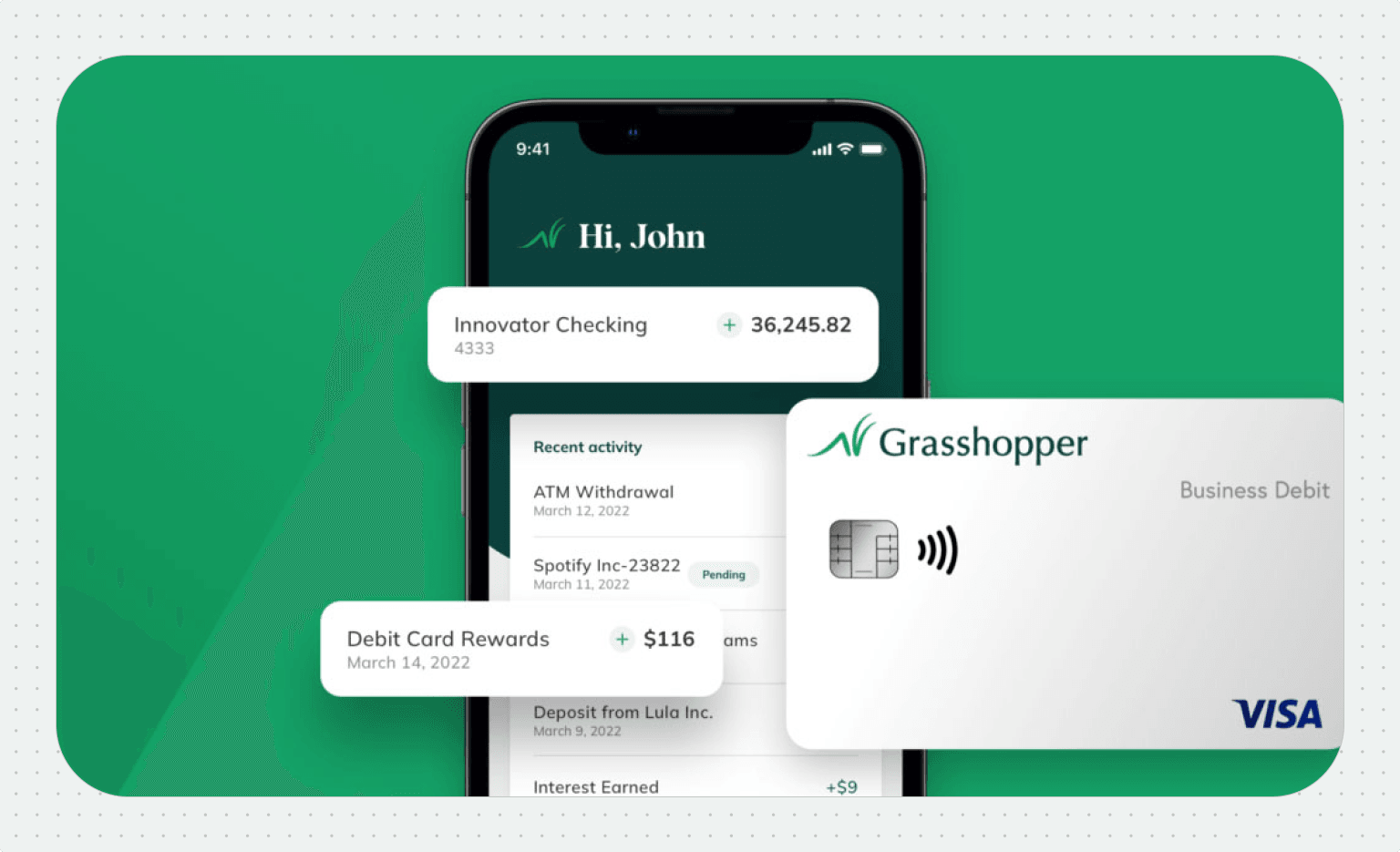

9) Grasshopper

Grasshopper is a federally chartered, FDIC-insured digital bank built specifically for startups and the innovation economy. Unlike fintech platforms that partner with banks, Grasshopper Bank, N.A. is itself a licensed bank — which means deposits are held directly at Grasshopper and protected under its own federal charter.

Its standout feature is extended FDIC coverage: up to $125 million through its ICS Deposit sweep network, placing it between Rho ($75M via ADM) and the standard $250K offered by most traditional and fintech banks. For a company holding significant post-raise cash balances, that coverage depth is material.

Grasshopper key features

Accelerator Checking — Interest-bearing business checking, unlimited transactions, free ACH and domestic wires, no monthly fees ($100 minimum to open)

Accelerator Savings — Up to 3.00% APY on balances of $25,000 or more (as of January 5, 2026; variable; subject to change)

Extended FDIC coverage — Up to $125M via ICS Deposit sweep network (Grasshopper Bank, N.A., Member FDIC)

Debit card — 1% cash back on online and in-store signature purchases

Business Bill Pay — ACH and check payments from the dashboard

Grasshopper Connect — Investor network access exclusive to Grasshopper startup clients

Accounting integrations — QuickBooks, Autobooks, Xero (Beta)

Venture lending — Up to $200K within one business day for banking clients; up to $5M for broader business needs; SBA lending available

Treasury portfolios — Target yields up to 5%+ for startup clients (variable; subject to change)

Grasshopper pricing

$0/month (no monthly fees)

$100 minimum to open an account

No fees on ACH or domestic wires

Honest assessment

Grasshopper sits in a distinct position on this list: it's a real bank (not a fintech with bank partners), with extended FDIC coverage that exceeds Mercury's $5M and approaches Rho's $75M. For a funded startup that wants to bank with an FDIC-chartered institution specifically focused on the innovation economy — with meaningful deposit protection and competitive savings yield — Grasshopper is worth serious evaluation.

The limitation: Grasshopper is primarily a banking product. It doesn't offer integrated corporate cards with cashback, expense management, AP automation, or the full spend management stack that Rho provides. The debit card's 1% cashback is lower than Rho's 1.5% corporate card. And at $720 million in total assets, Grasshopper is significantly smaller than Webster Bank (Rho's partner, $85.6B in assets) or First Citizens Bank (SVB's parent).

Best for: funded startups that want a startup-native chartered bank, extended FDIC coverage above $75M, high-yield savings, and investor network access — and are comfortable using a separate spend management tool for cards and expenses.

10) Capital One

![]()

Capital One is the largest card issuer in the United States and has been making an aggressive push into startup and business banking — most recently through its $5.15 billion acquisition of Brex, completed April 7, 2026. That acquisition is the clearest signal of where Capital One sees the market going: it bought its way into fintech-native spend management rather than building it from the ground up.

For founders, Capital One shows up in two contexts. First, as the business banking option for companies already in the Capital One ecosystem — existing Spark card holders, businesses with established Capital One lending relationships, or companies whose founders bank personally with Capital One. Second, as the institutional infrastructure now underpinning Brex, which means some founders are effectively on Capital One without having chosen it explicitly.

Capital One key features

Business Checking — Multiple tiers including Basic Business Checking ($0/month) and Unlimited Business Checking ($35/month)

Spark Business Cards — Spark Miles and Spark Cash rewards cards with travel and cashback options; Spark Cash Plus (charge card) with unlimited 2% cashback

Business Advantage Savings — Interest-bearing savings account

Brex (acquired) — Through the April 2026 acquisition, Capital One now owns Brex's corporate card, expense management, and spend management platform

Lending — Business lines of credit and term loans

Digital banking — Mobile and online banking, widespread ATM access

Capital One pricing

Basic Business Checking: $0/month

Unlimited Business Checking: $35/month (waivable with $25K average monthly balance)

Spark card annual fees: $0–$150 depending on card

Honest assessment

Capital One has been buying rather than building in the fintech space — the Brex acquisition is the most prominent example, but it reflects a pattern. Acquired tools stitched onto a legacy banking core is the definition of the patchwork problem Rho was built to replace.

The question for a founder isn't whether Capital One has the features. It's whether a bank that serves everyone from personal checking customers to Fortune 500 companies is actually built for a 12-person venture-backed startup that needs to open an account in 20 minutes and move a wire at midnight. The support model, onboarding speed, and integration depth reflect a product built for a much broader customer profile.

For founders who want rewards on a business credit card and already have a Capital One relationship, the Spark Cash Plus card (2% uncapped cashback) is genuinely competitive. For founders who want integrated banking, cards, bill pay, expense management, and treasury from a platform built specifically for startups — Capital One is not that platform. The right comparison is between the experience of a 10-person startup at Rho vs. the same company at a bank that serves 100 million personal customers.

Not ideal for: Founders choosing their first banking stack, pre-seed or seed-stage startups that want fintech-native speed, or companies that specifically chose Mercury or Rho to stay outside big-bank infrastructure.

Rho vs. Mercury: The head-to-head

Rho | Mercury | |

|---|---|---|

Business banking | Webster Bank, N.A. ($85.6B assets) | Fintech operating through partner banks: Choice Financial Group and Column N.A. Mercury Bank, N.A. received conditional OCC approval in April 2026 - charter not yet active |

FDIC coverage | Up to $75M via ADM network | Up to $5M via partner sweep network |

Corporate cards | Up to 1.5% cashback, no minimum balance, available from day one | 1.5% cashback IO Mastercard; available from day one; 1.5% cashback and monthly repayment both require $15K balance |

Bill pay | $0 platform fees | $0, available on all plans (per Mercury pricing page, May 2026) |

Expense management | Included, $0, no user caps, full AP automation | Cards, receipt matching, spend controls, and reimbursements included; free tier caps reimbursements at 5 users/month; no AP automation or multi-step procurement workflows |

Treasury / yield | Multi-asset portfolios, selectable modes, no minimum | Money market funds; $250,000 minimum balance required to access (per Mercury pricing page, May 2026) |

ACH fees | $0 same-day ACH | $0 domestic ACH |

Wire fees | $0 domestic wires | $0 domestic wires |

Accounting integrations | QuickBooks, NetSuite, Sage Intacct | QuickBooks and Xero enriched automations free on all plans; NetSuite categorizations on Pro only |

Per-user fees | $0 | $0 base / $29.90/mo Plus (annual) / $299/mo Pro (annual) |

Phone support | 24/7, under 1-minute response | No phone support on any tier |

Pre-EIN onboarding | Supported - account opens before EIN clears | Not supported; EIN document required at application |

Treasury minimum to start | No minimum balance required | $250,000 across all Mercury accounts |

Available at incorporation | Stripe Atlas + Clerky | Available, but no pre-EIN onboarding |

The short version: Mercury is the right tool if you need the fastest possible account setup through a clean fintech interface, and plan to add more capable spend management and AP automation tools separately as you grow.

Rho is the right tool if you want banking, cards, bill pay, treasury, expenses, and accounting in one platform - set up once and trusted as the company grows - with no balance threshold to unlock the card, no add-on tools as you scale, and a stronger institutional foundation under your cash.

Request a free demo → | Open an account →

How to choose

The question isn't which tool has the best feature list. It's which foundation you'll never have to rebuild.

If you're pre-seed and only need an account to receive your first wire - Mercury is fast, clean, and correct for that moment. Just know you'll revisit the decision when you need cards with spend controls, integrated expense management, AP automation, and a treasury that doesn't require $250K to access.

If you want to set up your financial foundation once and have it scale from pre-seed through Series B without migration - Rho is the answer. Same account, same cards, same platform from incorporation through your first finance hire.

If you're scaling globally with multi-entity complexity and need local currency card issuance - Brex is purpose-built.

If cash flow visibility through multiple budgeted accounts is the core pain - Relay.

If you already have a banking relationship and want spend management on top - Ramp.

If yield on operating cash and credit access are the priorities - Bluevine.

If you're a solo founder or freelancer with simple needs - Found or Novo.

If your company has 100+ employees and procurement governance is the bottleneck - Airbase.

If you need physical branches or a traditional lending relationship - Chase as a complement, not a replacement.

Evaluate total cost honestly. Most of these platforms have free entry points. Mercury's real cost surfaces in the $15K balance requirement to unlock monthly card terms, Mercury Pro ($299/month, billed annually) for enriched NetSuite automations and a relationship manager, and the $250K minimum to access treasury yield. Rho's $0 pricing covers the full stack.

Check support before you commit. Mercury has no phone support. For a founder discovering a failed payment on a Friday evening, that matters. Rho's support responds in under a minute, 24/7, from day one.

Ready to see it yourself?

Rho is built for founders who want a financial foundation they can set up once and trust as they grow — without juggling a bank, a card platform, and a spend management tool.

FAQs

Yes - Rho is built for founders from day one. Rho supports pre-EIN onboarding, so you can get started before your EIN clears.

The account opens in minutes. Corporate cards are issued immediately with up to 1.5% cashback and no minimum balance. Treasury is available from the same platform the moment your funding lands - with no minimum balance required, unlike Mercury Treasury which requires $250,000 across all accounts.

Support responds in under a minute from a real person, at no cost, starting on day one.

Rho is the best overall Mercury alternative for venture-backed startups. It includes everything Mercury does - checking, savings, treasury, and a card - plus bill pay, full expense management with AP automation, invoicing, and accounting integrations in one connected platform.

No $15K threshold to unlock cashback or monthly card repayments. No $250K balance requirement to access treasury yield. No per-user fees. No phone support wall.

Backed by Webster Bank, N.A., an $85.6 billion institution founded in 1935.

Mercury is a fintech banking product - checking, savings, treasury (requires $250K minimum balance, earns up to 3.65% yield), an IO Mastercard available from day one (daily repayment and no cashback until $15K balance, then monthly terms and 1.5% cashback unlock), basic expense management including receipt matching and card controls (reimbursements free for up to 5 users/month, above that requires a paid plan), and bill pay. Deposits are held at partner banks - Choice Financial Group and Column N.A. Mercury Bank, N.A. has conditional OCC approval but is not yet an active chartered bank.

Rho is an integrated banking platform - the same banking foundation plus corporate cards (no minimum balance), bill pay (free on all plans), full expense management with AP automation, invoicing, and accounting integrations at $0 per user.

Mercury gates enriched NetSuite automations behind Pro ($299/month, billed annually). Rho's full stack is $0. Mercury has no phone support. Rho responds in under a minute, 24/7.

Yes - Mercury has expense management including corporate card controls, receipt policies, receipt matching, and reimbursements (free for up to 5 active users/month). What Mercury doesn't include is AP automation, multi-step procurement approval workflows, or vendor invoice processing. For a team beyond five employees submitting reimbursements, a paid plan is required. Companies that need procurement governance or complex approval routing typically add separate tools.

Yes. Mercury is FDIC-insured through its partner banks - Choice Financial Group and Column N.A. - for up to $5M via sweep networks. Your deposits are held at those partner banks, not at Mercury itself.

Mercury received conditional OCC approval for Mercury Bank, N.A. in April 2026, but that charter is not yet active. FDIC and Federal Reserve approval are still required before Mercury Bank can legally operate.

Yes. Rho integrates directly with QuickBooks Online, as well as NetSuite, Sage Intacct, Microsoft Business Central, and other leading ERPs. Transactions, receipts, and expense data sync automatically, enabling a faster month-end close without manual data entry.

The honest answer is: before you have to. The right time to open a Rho account is at incorporation - before payroll, vendors, and a finance hire make switching a project. The second-best time is right after a round closes, when you have capital to protect and the mental bandwidth to set it up correctly. Most founders who move from Mercury to Rho do so when a finance hire joins and asks why banking, cards, expense management, and bill pay aren't fully integrated.

Mercury is FDIC-insured through its partner banks - Choice Financial Group and Column N.A., Members FDIC - for up to approximately $5M via sweep networks. Deposits are held at those partner banks. Mercury Bank, N.A. received conditional OCC approval in April 2026 but is not yet an active chartered bank.

By comparison, Rho offers up to $75M in FDIC coverage through the ADM partner bank network. For a startup that has raised $1M or more, the gap is material: $75M vs. $5M in deposit protection.

Mercury's free tier covers basic banking, card controls, receipt matching, and reimbursements for up to 5 users. Once you need enriched NetSuite automations, reimbursements for more than 20 users (Plus handles up to 20 at $29.90/month), or a dedicated relationship manager, you're on Mercury Pro at $299/month (billed annually).

Add a separate AP automation or procurement tool and you're looking at $400-$600/month to run a complete financial stack.

Rho provides banking, cards, bill pay, expense management with AP automation, treasury, and accounting integrations at $0 per user, per month - for any team size.

Rho serves over 5,000 customers managing more than $2B in AUM, including Perplexity, Dr. Squatch, and Rhode Skin, as well as more than ten publicly traded companies and hundreds of venture-backed startups.